Finance Minister’s Budget Promises Unfulfilled: Key Tax Incentives for Farmers and Startups Missing in Economic Bill

News Summary

Editorial Review Completed.

- Finance Minister Dr. Swarnim Wagle’s budget speech announced at least seven tax incentives targeting farmers, startups, and NRNs are absent from the economic bill.

- Despite budget announcements, incentives related to agricultural machinery imports, stock market, and Tilganga lens production have been excluded from the bill, thus will not be implemented.

- Although the minister declared capital gains tax in the stock market would be finalized, the bill has actually increased tax rates to 7.5% and 10%.

June 22, Kathmandu – Following the presentation of the economic bill in Parliament, Finance Minister Dr. Swarnim Wagle has come under criticism for altering tax rates in at least seven key areas. It has now been confirmed that the vital commitments made in his budget speech have not been included in the bill.

Notably, tax incentives aimed at farmers, startup entrepreneurs, and Non-Resident Nepalis (NRNs) to encourage investment and business, although announced in the budget, are missing from the economic bill.

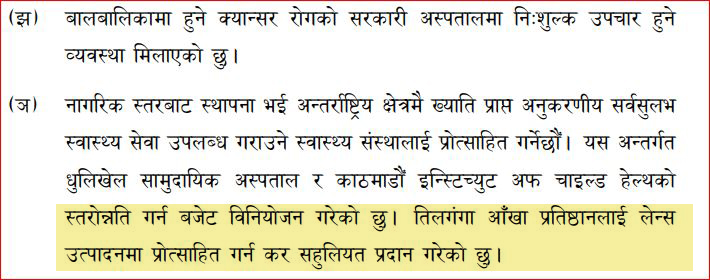

A promised tax concession for lens production by the Tilganga Eye Hospital is also absent from the bill. Since these incentives are not codified in law, they cannot be enforced.

Defending amendments on the ministry’s website after the bill’s parliamentary tabling, Minister Wagle repeatedly stated, “I mentioned in the budget speech that cinema halls outside metropolitan and sub-metropolitan areas will receive 10 years of income tax exemption, which was initially missed in the economic bill; that provision was subsequently added.”

While the bill now includes a 10-year income tax exemption for cinema halls outside major cities as originally announced, tax relief for farmers, also stated in the budget speech, was removed from the bill.

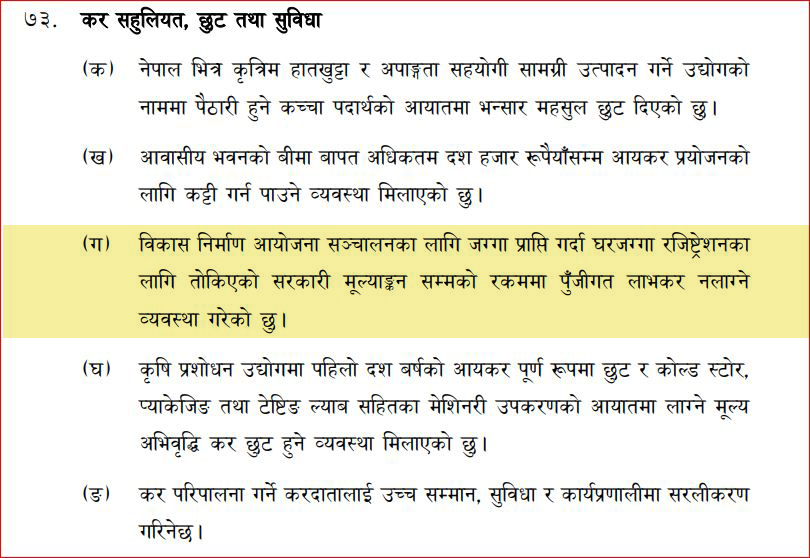

Point 73(g) of the budget states, “For agricultural processing industries, I have arranged a full 10-year income tax exemption and exemption from value-added tax on imported machinery including cold storage, packaging, and testing laboratories.”

However, the economic bill fails to provide value-added tax relief on the import of cold storage, packaging, and testing laboratory machinery.

This is just one of at least seven such announced incentives absent from the economic bill. Since they are not included in the bill, these budget commitments will not take effect.

To understand why this discrepancy occurs, it is important to recognize the legal status of a budget speech. Internationally recognized principles on revenue and spending state that “no taxation without representation” and “no spending without Parliament.”

Democratic countries enact legislative bills such as appropriation, economic, and national debt bills in Parliament, granting the government authority to tax and spend only after these bills pass.

While budget speeches cover key aspects in language understandable to the public, they do not legally bind tax or spending changes unless regulated through these bills. It is uncommon for matters absent from bills to be included in budget speeches.

Budget Speech Promises Missing From Economic Bill

Besides agricultural sector incentives, six other announced provisions are missing in the bill.

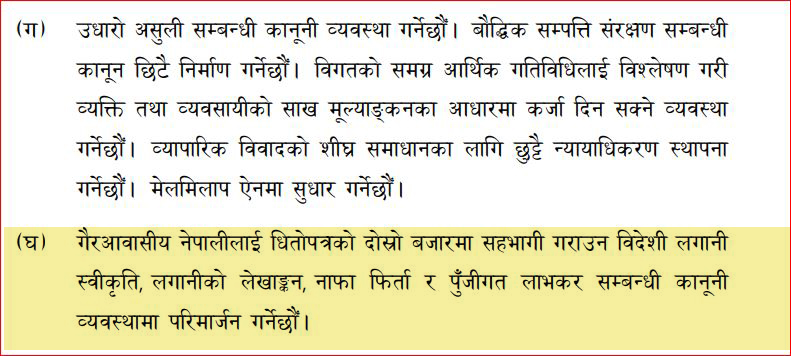

Second, point 10(घ) of the budget speech mentions: “To allow NRNs to participate in the secondary market (stock trading), we will amend laws relating to foreign investment approval, investment accounting, profit repatriation, and capital gains tax.”

While investment approvals and accounting may be handled by other laws, changes in capital gains tax must come via the economic bill, which has not occurred.

According to the Income Tax Act, non-resident individuals currently pay 25% capital gains tax. With the absence of promised revisions in the economic bill, senior Chartered Accountant Umesha Raj Pandey explains NRNs continue to face this 25% tax rate in Nepal.

“Section 67 of the Income Tax Act, 2058 defines immovable property in Nepal, excluding securities for non-residents, meaning capital gains from securities sales by NRNs are not considered Nepal-sourced income and therefore may not be subject to withholding tax, but this is not addressed in the bill,” Pandey explains.

Third, point 73(g) of the budget states, “When acquiring land for development projects, capital gains tax will not apply up to the government-assessed registration value.”

Although a tax concession was promised on land compensation for road and infrastructure construction by the government, it is not provided for in the economic bill.

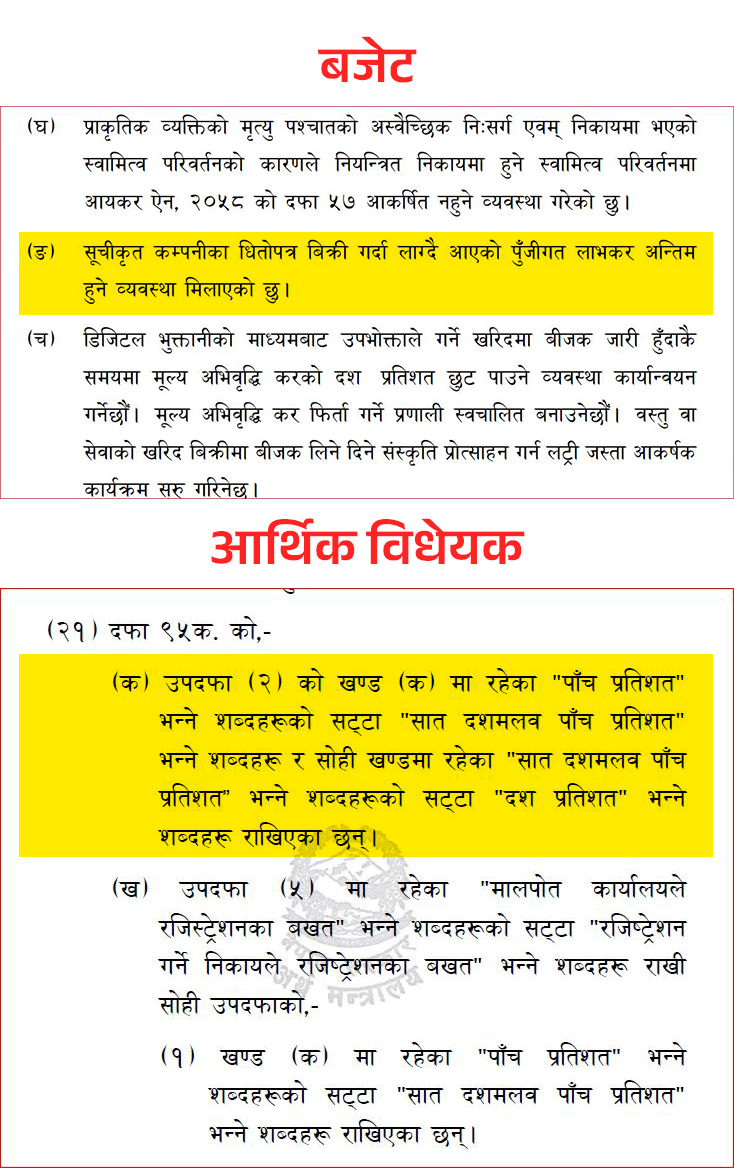

Fourth, the budget’s point 7(ङ) announces, “Capital gains tax on listed company securities sales will be final.”

Currently, investors may face income tax on capital gains even after paying capital gains tax, so there is a demand to declare capital gains tax as final.

Although the finance minister mentioned this in his budget speech, the bill has actually increased the tax rates to 7.5% and 10%.

Under previous rules, sales within one year were taxed at 7.5% and sales after holding longer received a 5% rate.

The bill’s amendments under section 95k of the Income Tax Act set capital gains tax at 7.5% and 10%, but without declaring the tax final.

Because the promised finalization of capital gains tax was not codified, disputes persist on whether this tax is final or not, says senior Chartered Accountant Pandey.

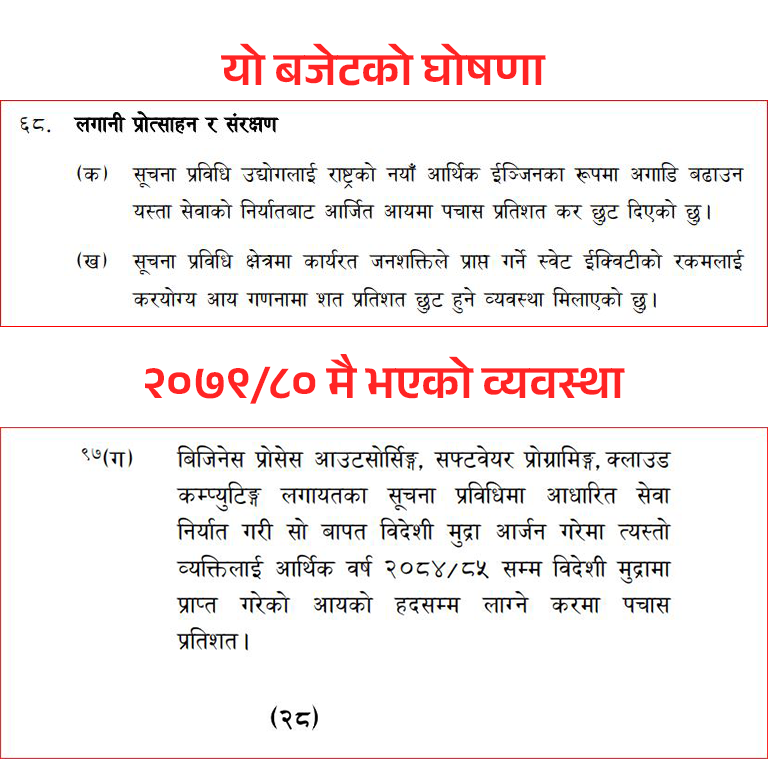

Fifth, point 68(ख) of the budget states, “I have granted 50% tax exemption on income from service exports to transform the IT industry into a new economic engine for the nation.”

This benefit was already granted by the Nepal government, but the minister claims credit for it. The new economic bill lacks any mention of this provision.

The 50% tax exemption for IT service export was first introduced in the economic bill of fiscal year 2079/80 (2022/23) and currently remains in effect.

Therefore, despite ministerial claims, the tax holiday is an existing one, not a new provision.

Sixth, point 74(ञ) of the budget speech states, “I have granted tax incentives on lens production to Tilganga Eye Hospital.”

However, this budget does not provide additional tax benefits to the Tilganga Eye Hospital for lens production as the economic bill contains no such provision.

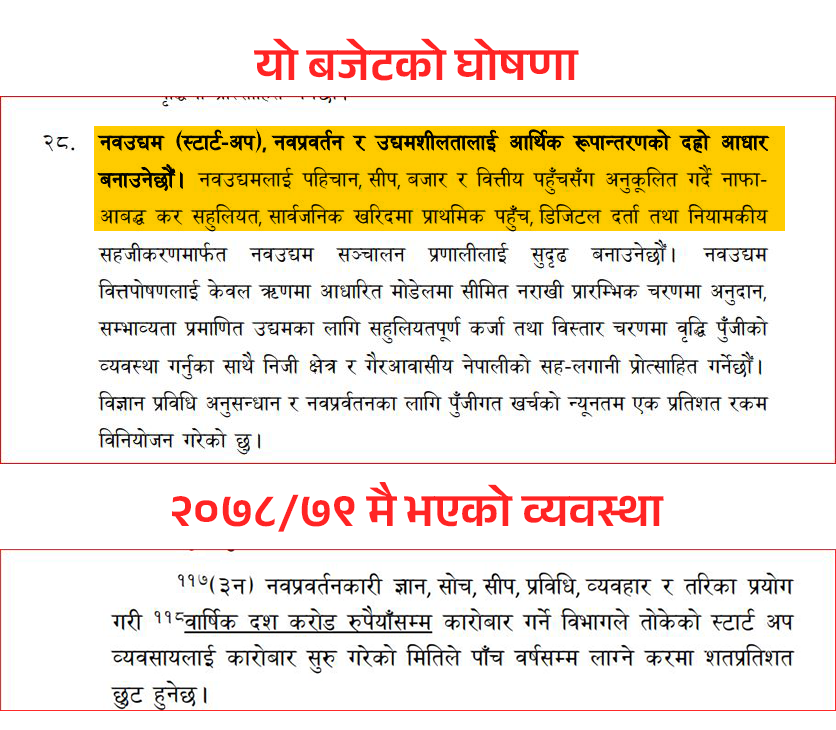

Seventh, point 28 of the budget speech states, “We will strengthen startup operations through profit-based tax incentives, priority public procurement, digital registration, and regulatory ease.”

Nepal does not have a tax called “profit-based tax,” so the intended reference may be to income tax relief. Nonetheless, no tax incentives for startups appear in this economic bill.

However, under section 11(3n) of the Income Tax Act, startups with annual turnover up to NPR 100 million that innovate receive 100% income tax exemption for five years, a provision preserved from earlier bills.

This provision remains unchanged this year, yet the finance minister has announced new profit-based tax incentives for startups without legislative backing.